TIF Information

From the Wisconsin Department of Revenue - Tax Incremental Financing (TIF) Manual

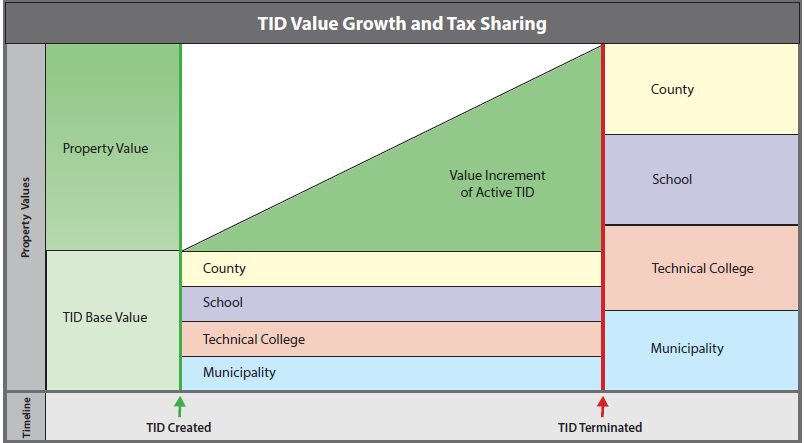

TIF basic function: TIF is a financing option that allows a municipality (town, village or city) to fund infrastructure and other improvements, through property tax revenue on newly developed property. A municipality identifies an area, the Tax Incremental District (TID), as appropriate for a certain type of development. The municipality identifies projects to encourage and facilitate the desired development. Then as property values rise, the municipality uses the property tax paid on that development to pay for the projects. After the project costs are paid, the municipality closes the TID. The municipality, schools, county, and technical college are able to levy taxes on the value of the new development.

TIF use varies depending on the project and the municipality. In some cases, the municipality chooses an area it would like to develop or that is unlikely to develop without assistance. Then the municipality designs improvements (ex: roads, sidewalks, sewer systems) to attract growth. In other cases, a developer or company identifies a site where they might locate. A developer may also negotiate with the municipality to use TIF to fund some improvements (ex: demolition, soil clean up, roads, water) the developer needs. Either way, an area facing development challenges receives help to grow. This creates a larger tax base for the municipality and the overlying taxing jurisdictions (ex: schools, county, technical colleges). Generally, when the tax base grows and spending is stable, tax rates go down, decreasing property taxes for everyone.

Important:One key basis for the use of TIF is the "but for" requirement. As part of all creation resolutions, a municipality must affirm that the development would not happen "but for" the use of TIF. The municipality must believe that without TIF the development would never happen. This requirement is important to ensure TIF assists development projects needing help, but that it is not a gift of tax dollars to private developers or property owners. Review Considerations for the Municipality for more information.

TIF law background: Wisconsin adopted TIF legislation in 1975 to eliminate blighted areas in urban neighborhoods. Interest rates were high, making government borrowing expensive and municipal investment in infrastructure and redevelopment unattractive. In addition, the cost was high for redeveloping blighted areas compared to developing open areas. This was due to demolition, alteration, remodeling or repairing existing buildings, removing environmental contamination from soil or groundwater, or other site work. Before TIF law was enacted, if a municipality wanted to expand its local tax base, the municipality alone would pay the cost but the overlying taxing jurisdictions would also benefit from the growth. The legislature saw this situation as unfair and viewed TIF as a way to remedy the problem and encourage cooperation between local government.

Since TIF law was first adopted, changes have been made to expand the ways municipalities can use TIF and increase the involvement of the overlying taxing jurisdictions and local residents.

Below is a helpful Visual on how a TID/TIF works.

| Attachment | Size |

|---|---|

| 1.58 MB | |

| 3.85 MB | |

| 1.12 MB | |

| 6.54 MB | |

| 1.23 MB |